Is natural gas still a financial no-brainer?

For more than a decade, natural gas has been promoted as a “bridge fuel” in the energy transition. But the choice comes with both an economic and environmental compromise.

Natural gas is no immune to climate risk, policy uncertainty, and volatile global markets. Although it’s generally cheaper than oil and releases fewer emissions than coal, a huge dependency on gas infrastructure can potentially slow the shift to fully renewable systems.

While it may play a transitional role to renewable sources, its long-term impact depends on how quickly we scale up low-carbon alternatives, manage methane leaks and its environmental risks.

Read: Is natural gas renewable or non-renewable?

But natural gas looks like a financial no-brainer

Unlike oil, natural gas prices have steadily declined between 2005 and 2020, especially in the U.S., since it replaced coal. The average price reached toUSD 3.33/MMBtu in 2023, compared to USD 6.42/MMBtu in 2022.

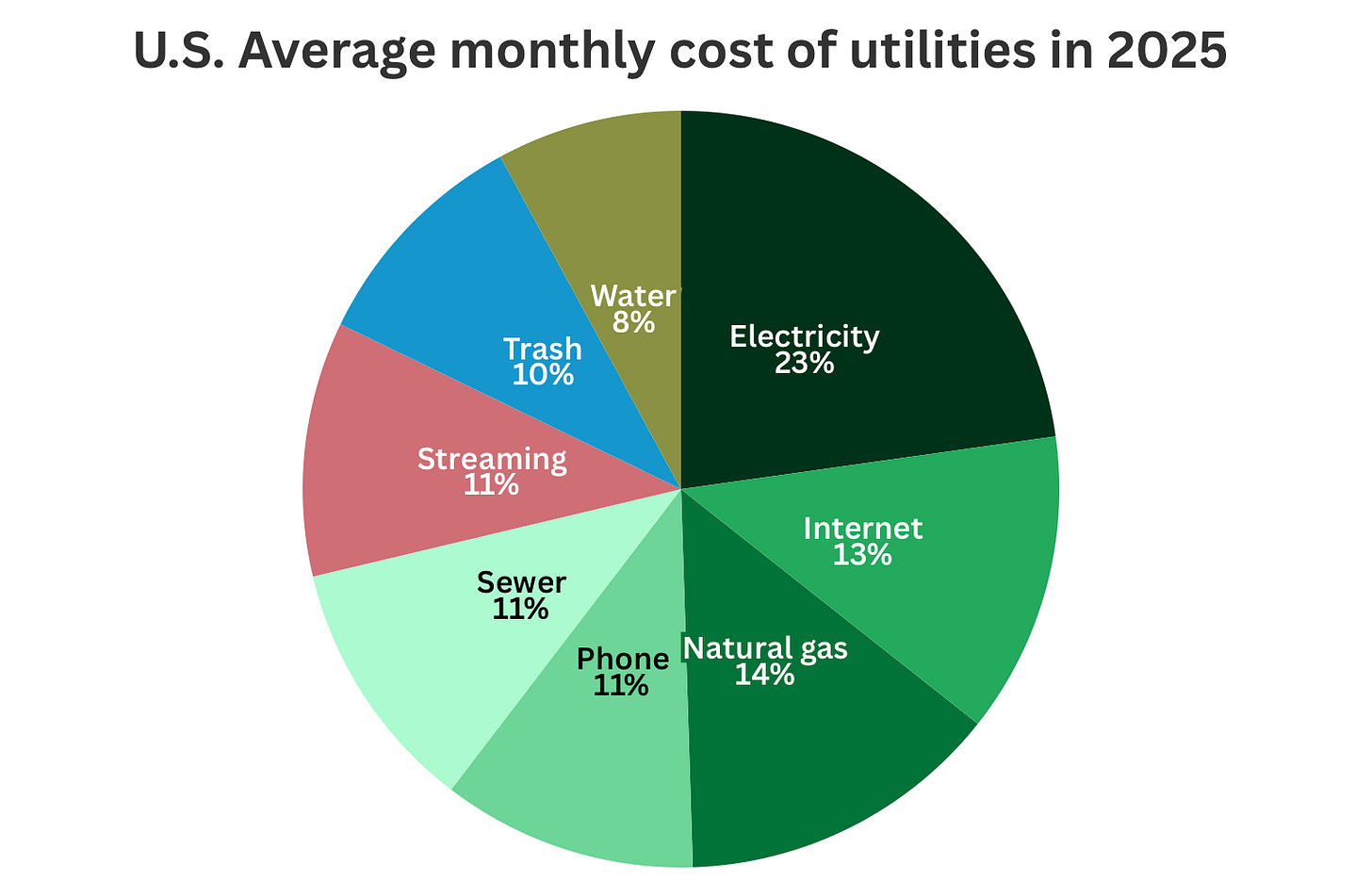

A recent Move.org report indicates that the average monthly U.S. utility bill (electricity, natural gas, and sewer) is approximately USD 401, with total utilities (including additional services) reaching around USD 611 per month. As shown in Figure 1, natural gas accounted for roughly 14% of total utility costs in 2025.

One of the main reasons natural gas is so popular is that it is usually easier to handle. Utilities could deploy them quickly, investors have predictable cash flows, and policymakers viewed gas as a way to reduce emissions. For everyone, it is a win-win situation. It costs less, emits less, and has a stable return.

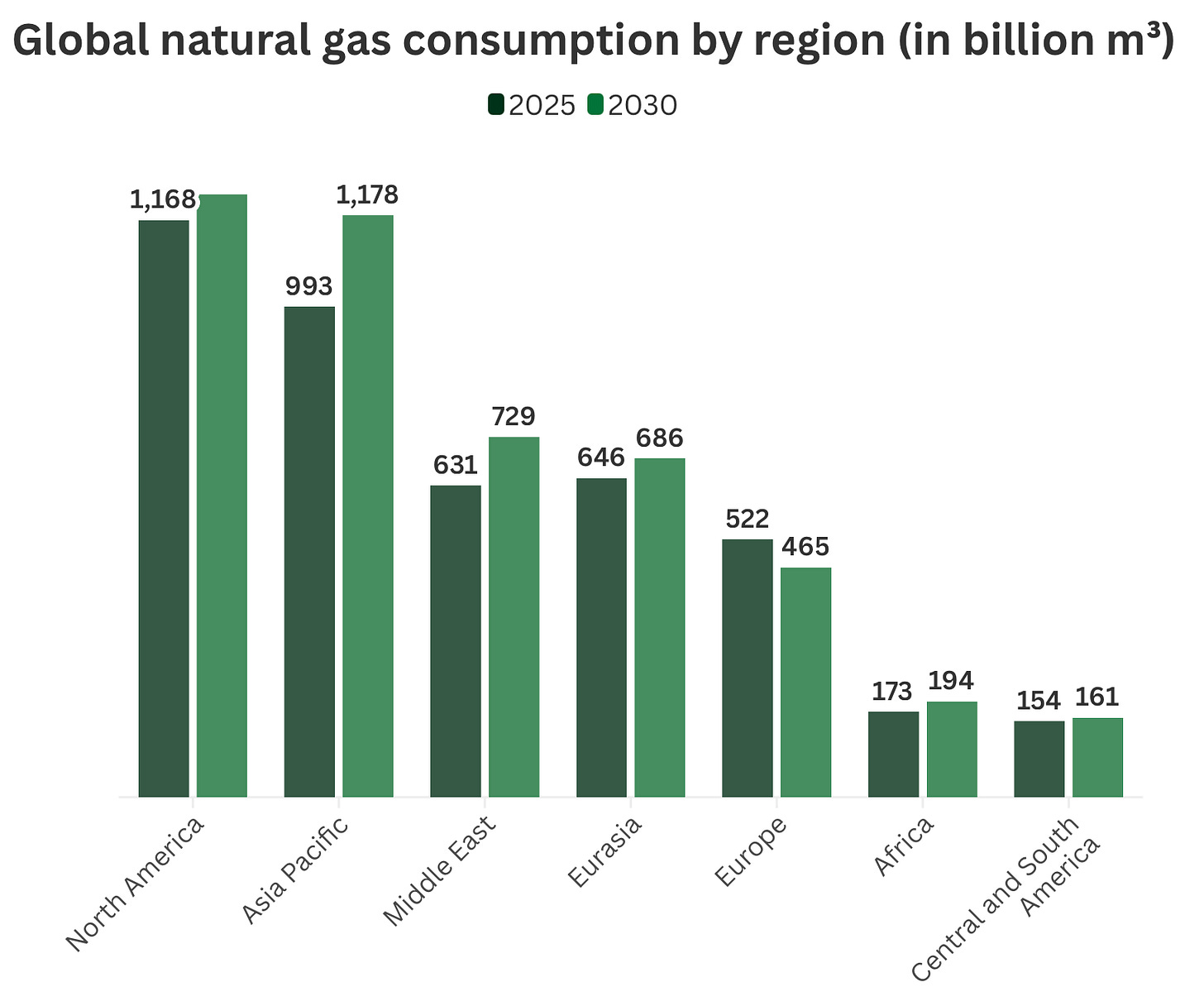

This is also the main reason the natural gas consumption is expected to go up in 2030, compared to 2025 (Figure 2). The U.S. Energy Information Administration in 2016 estimated that shale gas would account for 30% of world natural gas production by 2040.

The price volatility and infrastructure

Unlike renewables, which have high upfront costs but near-zero fuel expenses, gas prices are exposed to commodity cycles, geopolitics, weather, and global demand.

For example, the 2021–2022 energy crisis showed how quickly gas prices can spike when supply chains tighten. For utilities, this volatility translates directly into higher operating costs. When that happens, it is a higher electricity and heating bills for households.

Another concern is the long-lived infrastructure that natural gas relies on. The pipelines, processing plants, storage facilities, and gas-fired power stations are designed to operate for 30–40 years. However, shifting climate priorities and changing energy policies can shorten the useful economic life of these assets, creating the risk of early devaluation and stranded investments for owners and utilities.

As renewables and battery storage become cheaper, gas plants are increasingly used for peak demand only. That means lower utilisation rates but the same fixed costs. Pipelines built today may not recover their investment if demand declines faster than expected. This creates the risk of infrastructure still existing physically but no longer generating sufficient revenue.

Read: The critical role of power sources in the climate crisis

Methane is the hidden financial risk

Methane leaks are often discussed as an environmental issue, but they are equally a financial one, too.

A new study published in Nature finds that U.S. oil and natural gas operations are emitting three times more methane than the government estimates, causing about USD 9.3 billion in annual climate damage. Researchers estimate that roughly 3% of U.S. gas production is leaking, compared with the Environmental Protection Agency’s 1% estimate.

Since 2021, pressure to cut methane has intensified. At COP28 in 2023, companies representing about 50% of global oil production signed the Oil & Gas Decarbonization Charter, pledging to achieve near-zero methane emissions and zero routine flaring by 2030.

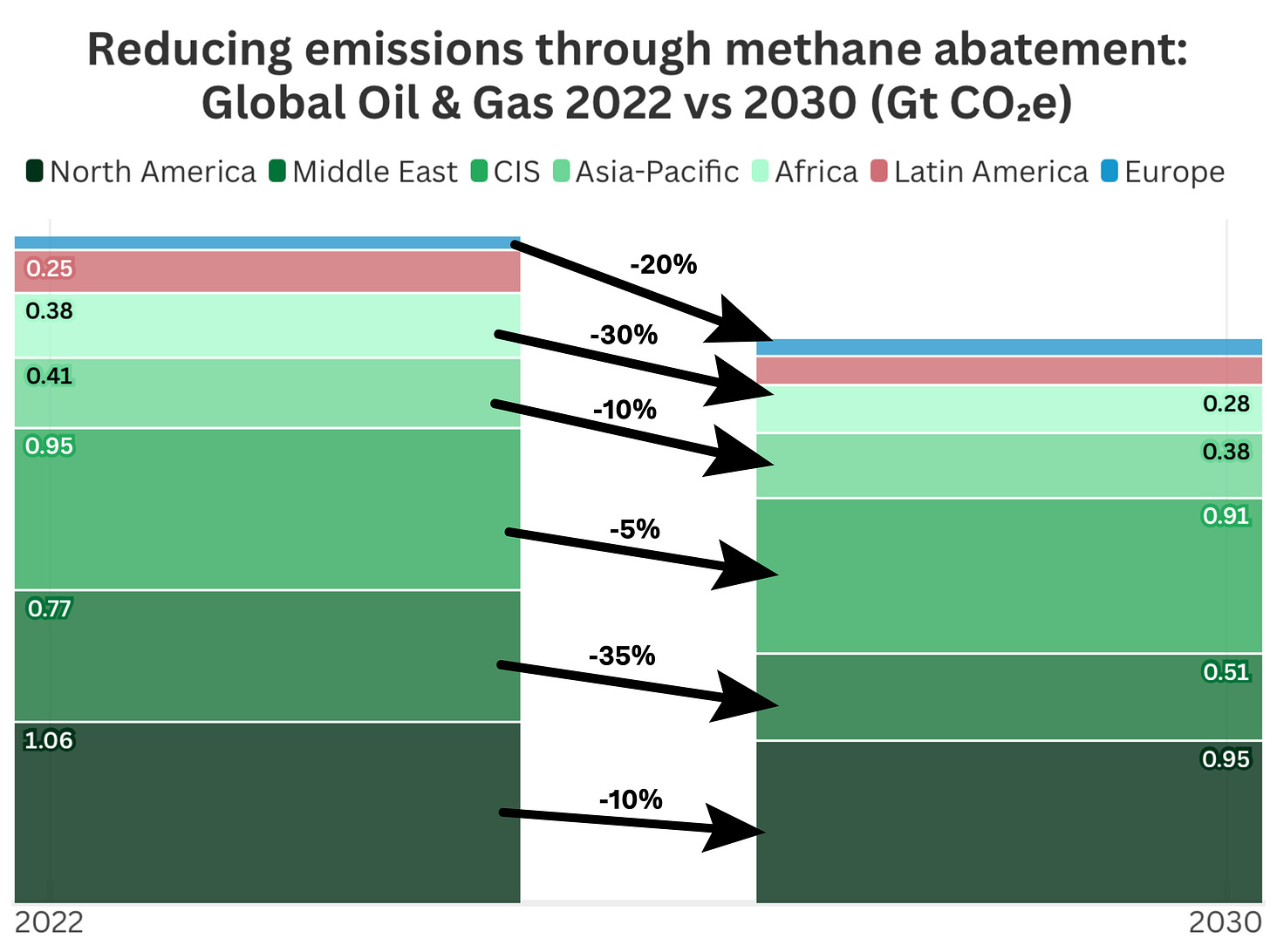

The pledge was signed by more than 50 companies, including many of the world’s largest. Meeting these targets will reduce emissions by 0.6 GtCO2e per year by 2030, which corresponds to a 15% decline, compared to 2022 in total upstream Oil & Gas emissions (Figure 3).

However, achieving this would require major investment. An estimated USD 200 billion in total capital would be needed, including about USD 120 billion for infrastructure such as pipelines, LNG terminals, and transport systems to bring captured methane to market.

How natural gas compares to renewables

From a cost perspective, renewables have crossed a critical threshold. Utility-scale solar and wind are now among the cheapest sources of new electricity generation, even without subsidies. Battery storage costs continue to fall, reducing reliance on gas for grid balancing.

Natural gas still plays a role in reliability, but its comparative advantage is shrinking. As renewables become cheaper and more predictable, gas increasingly functions as a hedge rather than a growth engine.

For investors, gas offers shorter-term cash flow stability but weaker long-term growth. Renewables offer higher upfront risk but stronger long-term visibility. The real question isn’t whether natural gas is profitable today but whether it remains profitable over the lifetime of the asset.

So, does natural gas still make sense?

Financially, natural gas is no longer the obvious answer it once was. It can still generate returns, but those returns come with higher risk and tighter margins.

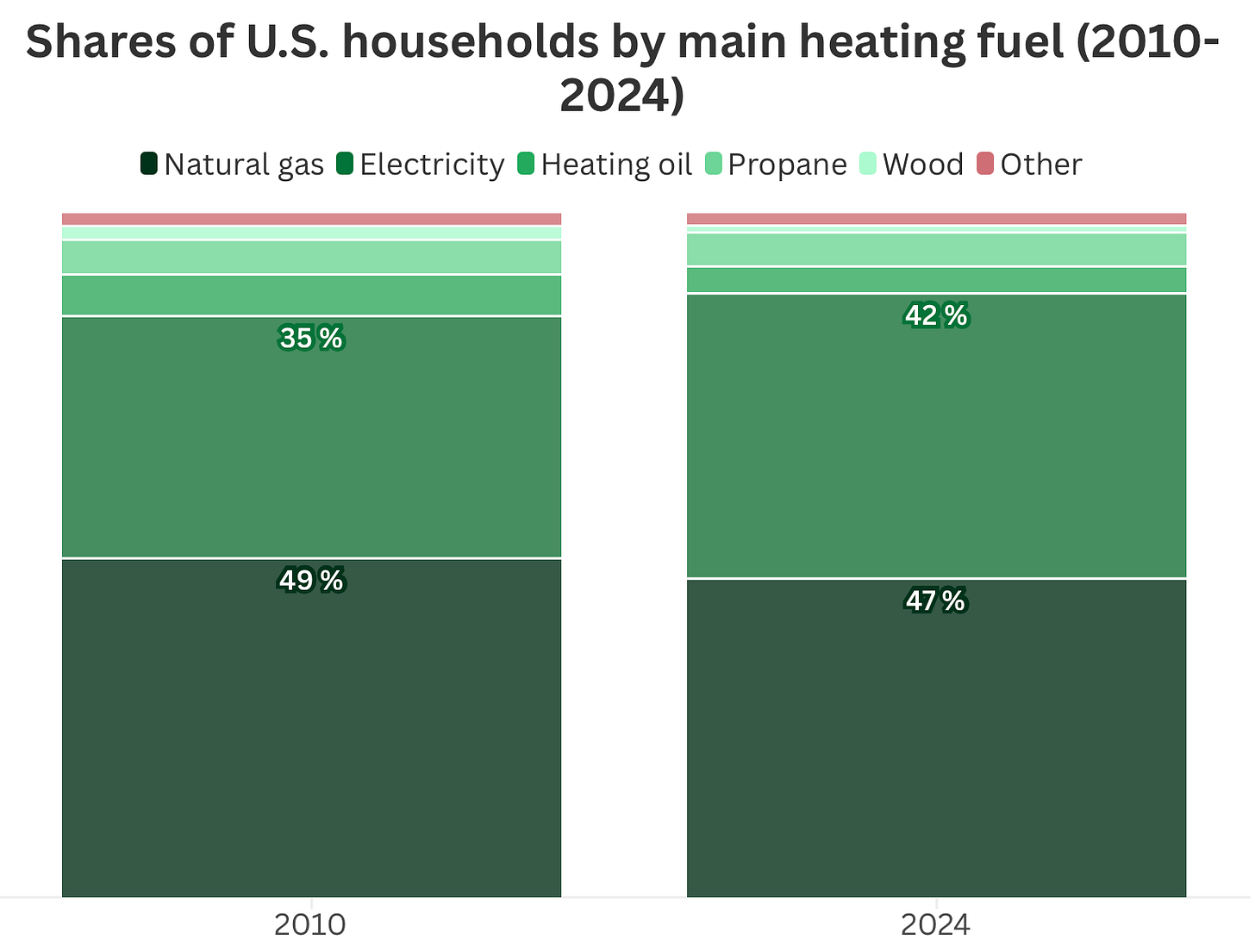

Figure 4 shows that about 47% of the U.S. households were using natural gas as a main heating fuel in 2024, which is only 2% down in 14 years. It’s less likely that there will be a drastic change in these numbers in the next 10 years, but it is important to understand that renewables now offer what gas once promised: cost stability, scalability, and long-term relevance.

One research study in 2023 stated that natural gas plays an important role in assisting in the transition to renewables, but the world may not produce enough natural gas each year to meet demand by 2050.

However, the challenge is not the amount of gas, but investing enough money to develop and produce it. If that investment happens, natural gas can remain widely available and help support as a bridge to renewable energies.