Are climate disasters destroying our real estate wealth?

According to the Investment Intentions Survey in Jan 2026, 38% of investors plan to increase real estate investment over the next two years. However, ShelterBox warns that rising extreme weather could lead to the loss of 8.35 million homes annually until 2040.

A well-known way to invest savings has been buying a property and renting it out, a strategy widely used, especially by the baby boomer generation. While all investments carry risk, the disparity between climate realities and financial values is particularly clear in the property insurance market.

For most people, real estate isn’t just an investment; it's their personal wealth, retirement plans, and financial security. So, losing a house to extreme weather is devastating, but when that happens, the impact is both painful and compounding because the rising insurance costs also steadily drain savings.

Read: Climate-linked disasters costing billions: insurers urged to act to avoid catastrophe

The insurance problem is the first crack

The clearest signal that climate risk is hitting real estate isn’t coming from governments or investors. It’s coming from insurers.

According to ABI’s latest data, insurers paid out £6.1 billion in property claims in 2025 in the UK. That is the highest annual total on record. The director of General Insurance Policy at the ABI, Chris Bose said:

“Once again, we’re seeing the toll that increasingly severe weather is taking on homes and businesses across the UK. A record £6.1 billion in property claims last year shows both the scale of the damage and the vital role insurers play in helping people recover.”

In Figure 1, we can see the global data on economic damage from 2024. Natural disasters caused about USD 320 billion in losses, of which only 43.8% were insured.

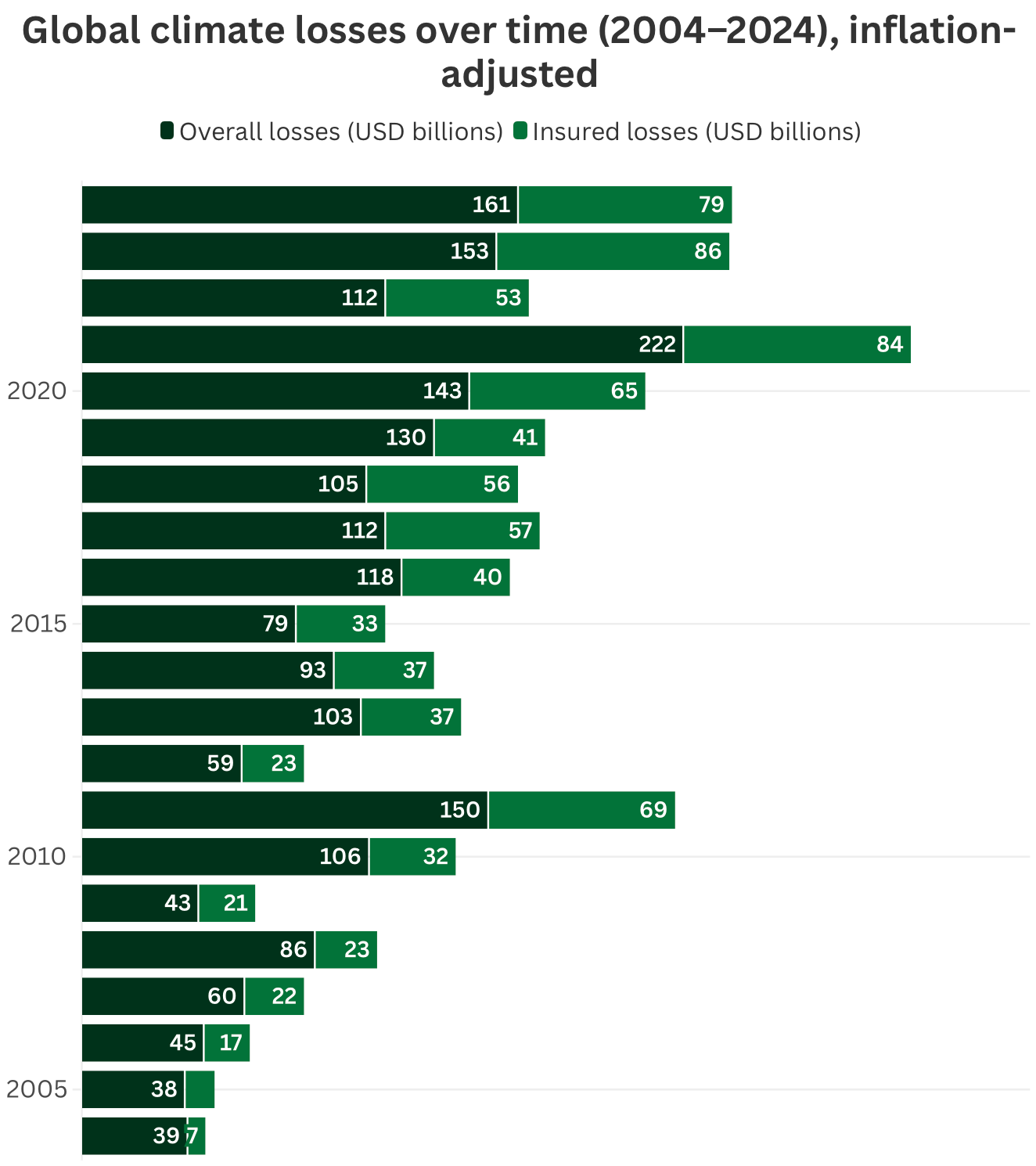

Figure 2 shows global climate-related losses over the 20-year period from 2004 to 2024. The year 2021 recorded exceptionally high losses from natural disasters, with Hurricane Ida being one of the major contributors.

For insurance companies, it was one of the most costly years on record, even though only around 38% of the losses were insured.

Key climate risk categories

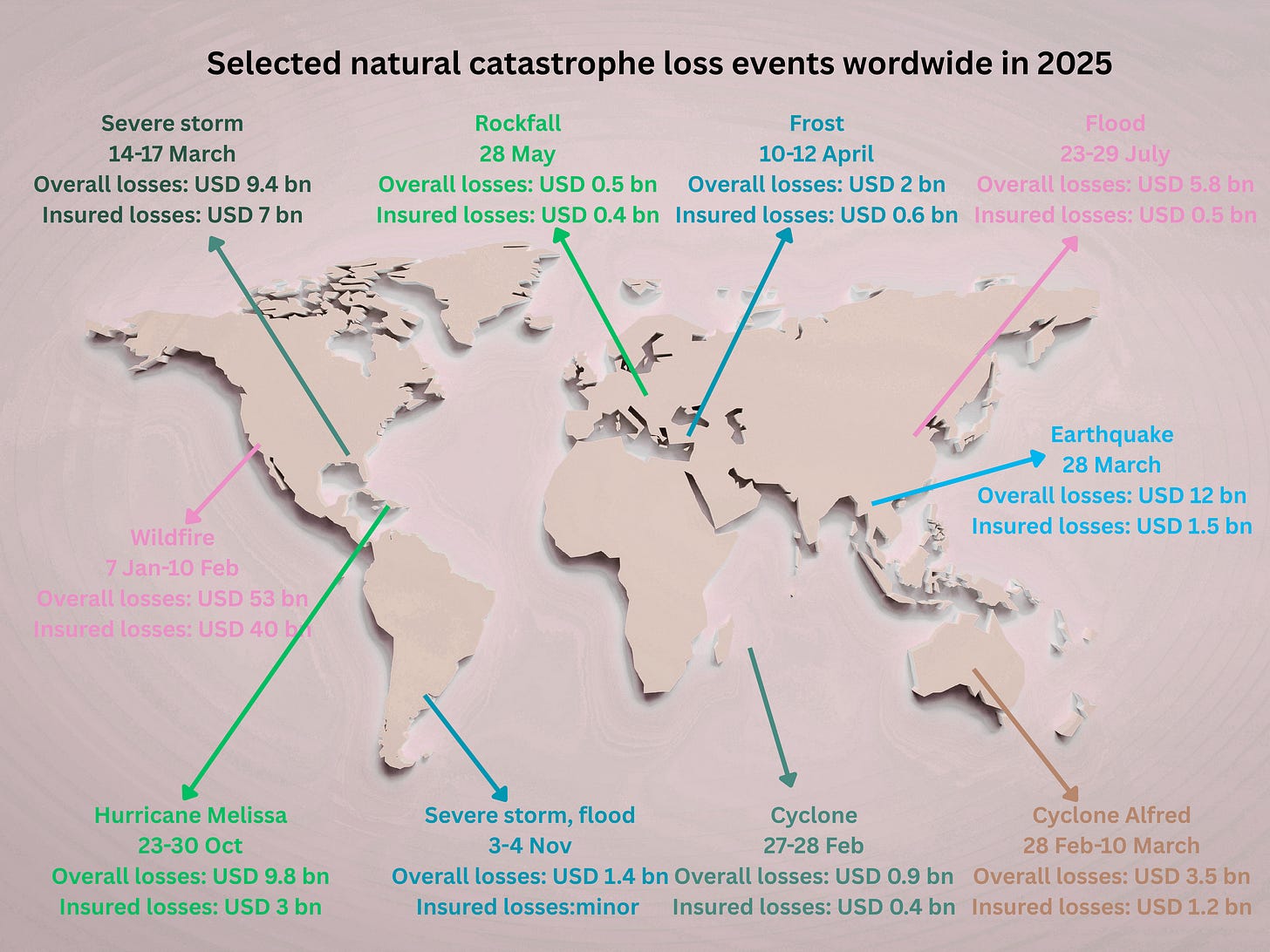

Climate risk becomes far more tangible when viewed through real estate. Figure 3 shows selected natural catastrophe events around the world in 2025 and the financial losses caused by their impacts.

In high-risk areas, this often leads to higher future insurance premiums as properties are reclassified as more exposed. Insurance risk can be grouped into several categories:

- Physical risk refers to damage from floods, wildfires, and heat. These events do not only create one-off repair costs; they can reduce long-term property value. A home that floods repeatedly becomes harder to insure, harder to sell, and less attractive to buyers.

- Transition risk comes from regulation and changing building standards. Governments are tightening energy efficiency requirements, introducing retrofit obligations, and in some cases penalising inefficient buildings. Properties that fail to meet these standards may require costly upgrades before they can be sold or rented.

- Liability risk is emerging more gradually but is increasingly important. Developers, landlords, and even public authorities may face legal and financial consequences for building or maintaining properties in high-risk areas or failing to disclose climate exposure. This feeds back into property pricing and financing conditions.

- Systemic risk links everything together. Real estate markets depend on insurance, mortgage availability, and stable valuations. If one of these pillars weakens, the whole system is affected.

For real estate, these risks are always present, but market stability depends on the ability to insure, finance, and eventually sell a property. In high-risk areas, rising insurance costs can reduce banks’ willingness to issue mortgages and that brings down the property values. What begins as an insurance issue quickly becomes a pricing issue.

How climate risk in property could impact your investments

Even if you don’t think of yourself as a property investor, you probably are. Pension funds and institutional investors hold large amounts of real estate, including office buildings and housing.

Many of these properties are exposed to climate risks such as rising sea levels in coastal areas, extreme heat in cities, and more frequent flooding in vulnerable regions. If these assets lose value, it can reduce long-term returns.

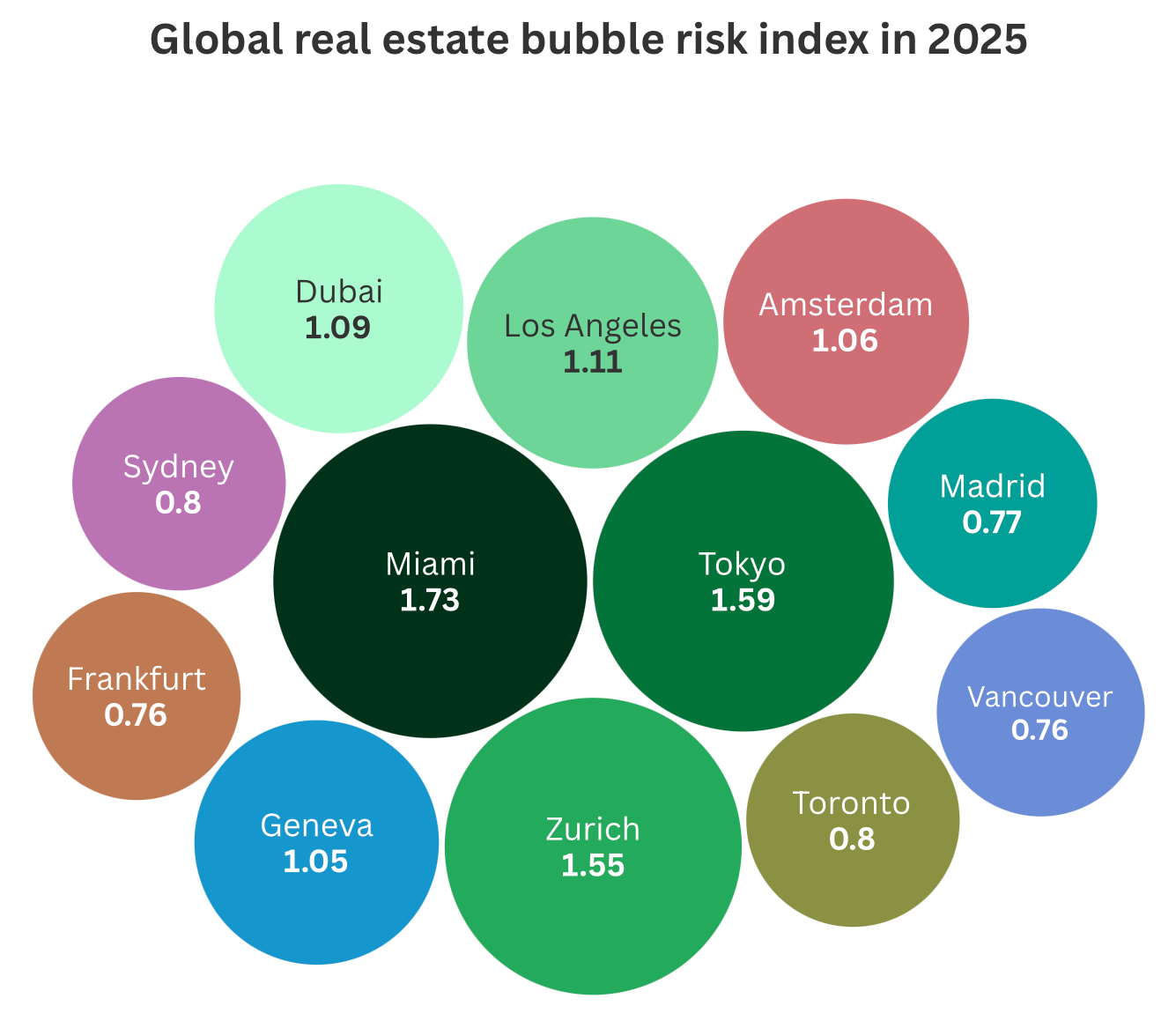

Figure 4 shows cities with the highest bubble risk according to the Global Real Estate Bubble Index 2025. The index uses indicators such as price-to-income ratios, price-to-rent ratios, mortgage lending trends, and construction activity. Cities are grouped into two categories:

- Bubble risk: above 1.5

- Overvalued: 0.5 to 1.5

Bubble risk is harmful for all market participants. It creates severe volatility in asset valuations and increases the likelihood of mispricing risk when the bubbles burst. When this happens, real estate values can fall sharply. During the 2008 financial crisis, UK house prices fell by approximately 14.7%.

While a fall in house prices may seem attractive for buyers with significant cash, for those relying on mortgages it often comes with higher borrowing costs and stricter lending conditions. In extreme cases, markets can partially freeze. Properties may become unmortgageable, which means there will be fewer buyers and longer selling times.

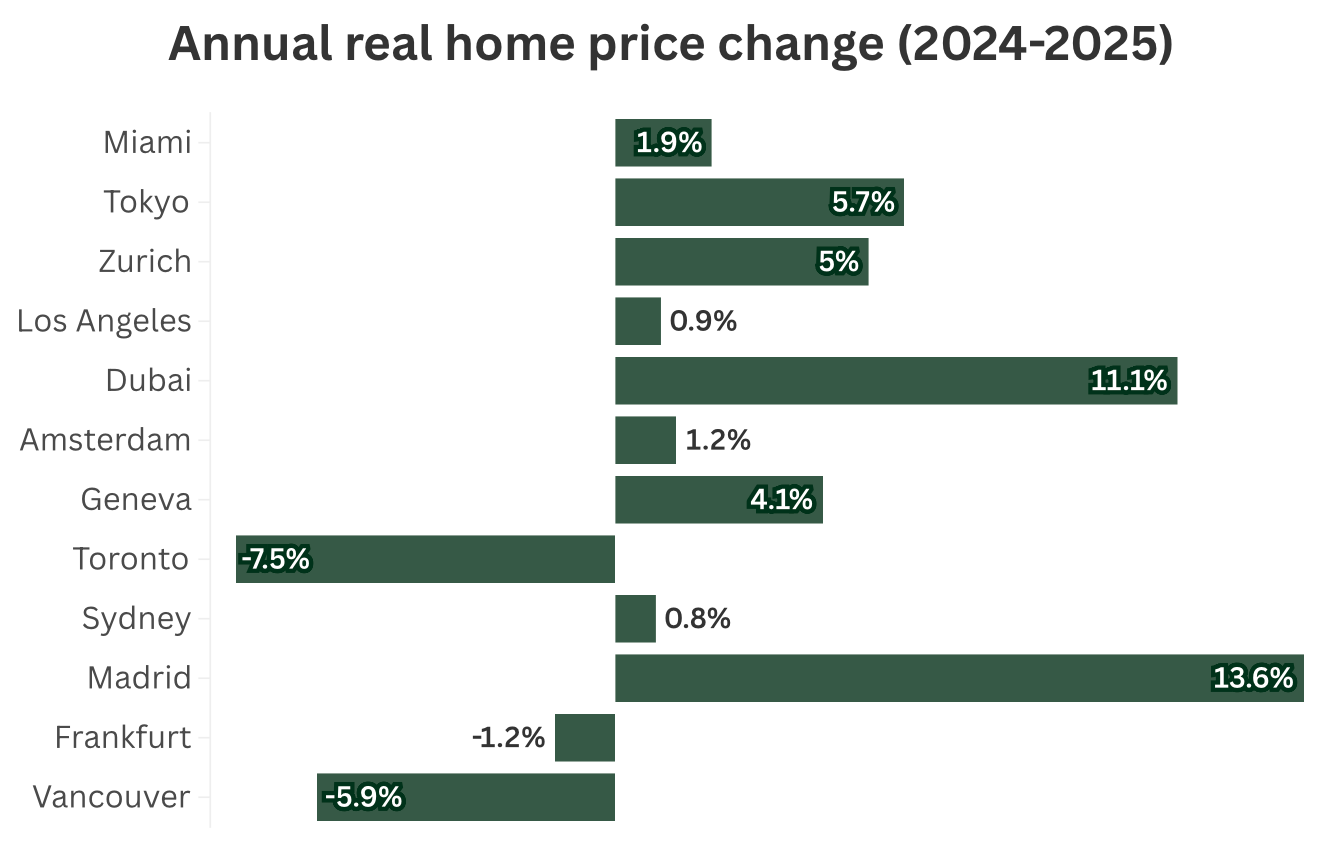

This is how climate risk feeds into financial risk: even without physical damage, it can weaken confidence in the market and put downward pressure on property values. Figure 5 shows house price changes in selected locations around the world between 2024 and 2025.

Imagine a typical four-bedroom house in Madrid valued at €700,000–€900,000. If a major flood hits and damages the ground floor and electrics, repairs could cost around €60,000–€80,000.

After the homeowner makes an insurance claim, the insurer reassesses the risk and may raise the annual premiums from about €800 to €2,000 or more. As a result, the property’s value could fall by 5–15%, depending on how often and how severely flooding occurs.

Read: How climate change is increasing your household bills

Property has long been seen as a reliable way to build wealth, but climate change is starting to challenge that view. Climate exposure has become a financial factor, not just an environmental one.

That means, we should start looking closely at local risks, such as weather patterns, insurance trends, as well as stricter energy efficiency rules and indirect exposure through pensions or investments linked to real estate. As these systems shift, they directly affect the value of our major assets.